Buying a Home Right Now: Easy? No. Smart? Yes.

Through all the volatility in the economy right now, some have put their search for a home on hold, yet others have not. According to ShowingTime, the real estate industry's leading showing management technology provider, buyers have started to reappear over the last several weeks. In the latest report, they revealed:

“The March ShowingTime Showing Index® recorded the first nationwide drop in showing traffic in eight months as communities responded to COVID-19. Early April data show signs of an upswing, however.”

Why would people be setting appointments to look at prospective homes when the process of purchasing a home has become more difficult with shelter-in-place orders throughout the country?

Here are three reasons for this uptick in activity:

1. Some people need to move. Whether because of a death in the family, a new birth, divorce, financial hardship, or a job transfer, some families need to make a move as quickly as possible.

2. Real estate agents across the country have become very innovative, utilizing technology that allows purchasers to virtually:

- View homes

- Meet with mortgage professionals

- Consult with their agent throughout the process

All of this can happen within the required safety protocols, so real estate professionals are continuing to help families make important moves.

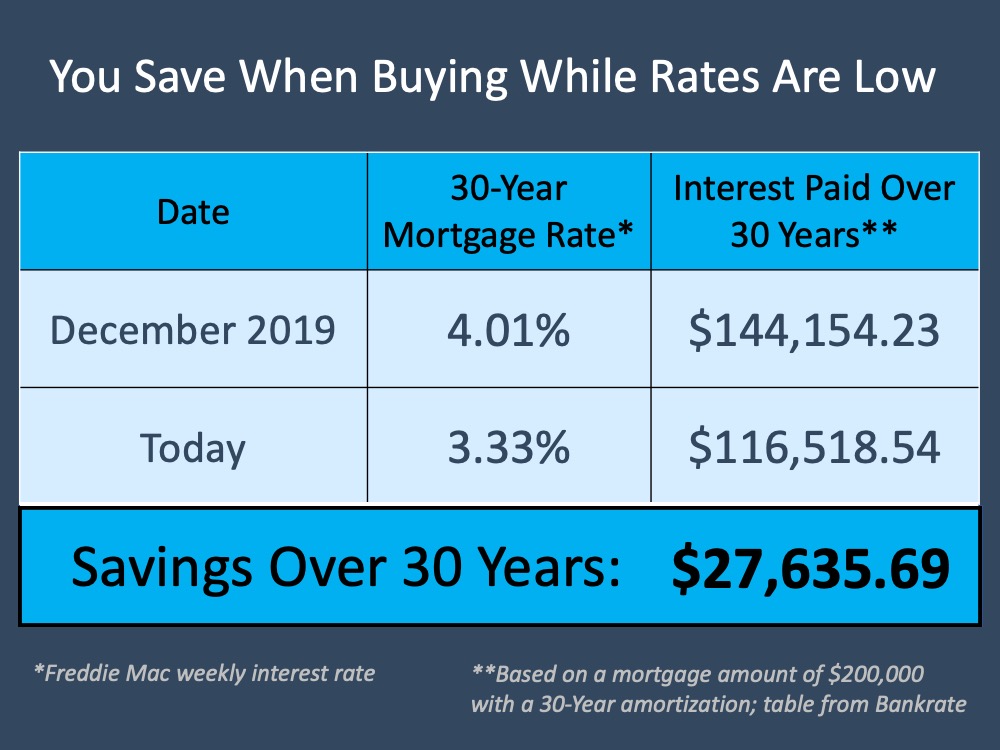

3. Buyers understand that mortgage rates are a key component when determining their monthly mortgage payments. Mortgage interest rates are very close to all-time lows and afford today’s purchaser the opportunity to save tens of thousands of dollars over the lifetime of the loan.

Looking closely at the third reason, we can see that there’s a big difference between purchasing a house last December and purchasing one now (see chart below):

Bottom Line

Many families have decided not to postpone their plans to purchase a home, even in these difficult times. If you need to make a move, let’s connect today so you have a trusted advisor to safely and professionally guide you through the process.

![Today’s Expert Insight on the Housing Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2020/04/23123713/20200424-MEM-EN-1046x1308.jpg)